- Автоматизация

- Антропология

- Археология

- Архитектура

- Биология

- Ботаника

- Бухгалтерия

- Военная наука

- Генетика

- География

- Геология

- Демография

- Деревообработка

- Журналистика

- Зоология

- Изобретательство

- Информатика

- Искусство

- История

- Кинематография

- Компьютеризация

- Косметика

- Кулинария

- Культура

- Лексикология

- Лингвистика

- Литература

- Логика

- Маркетинг

- Математика

- Материаловедение

- Медицина

- Менеджмент

- Металлургия

- Метрология

- Механика

- Музыка

- Науковедение

- Образование

- Охрана Труда

- Педагогика

- Полиграфия

- Политология

- Право

- Предпринимательство

- Приборостроение

- Программирование

- Производство

- Промышленность

- Психология

- Радиосвязь

- Религия

- Риторика

- Социология

- Спорт

- Стандартизация

- Статистика

- Строительство

- Технологии

- Торговля

- Транспорт

- Фармакология

- Физика

- Физиология

- Философия

- Финансы

- Химия

- Хозяйство

- Черчение

- Экология

- Экономика

- Электроника

- Электротехника

- Энергетика

General Standards

General Standards

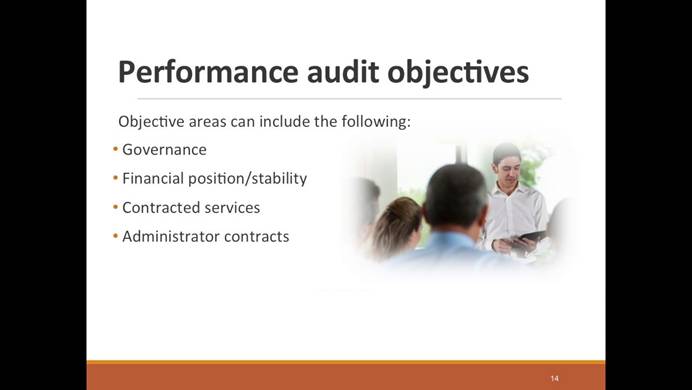

The general standards that guide government auditors, as well as other independent auditors, stated in summary style, are:

· Independence: The auditor and his/her firm must be free, in both fact and appearance, from all types of impairments of independence.

· Professional judgment: The auditor should use professional judgment in planning and performing all audits.

· Competence: Those individuals assigned to the audit must possess adequate professional competence for the tasks required to complete the engagement.

· Quality control and assurance: Audits must be performed by auditors whose organizations maintain an internal quality control system and have an external peer review on a regular basis.

|

|

|

© helpiks.su При использовании или копировании материалов прямая ссылка на сайт обязательна.

|