- Автоматизация

- Антропология

- Археология

- Архитектура

- Биология

- Ботаника

- Бухгалтерия

- Военная наука

- Генетика

- География

- Геология

- Демография

- Деревообработка

- Журналистика

- Зоология

- Изобретательство

- Информатика

- Искусство

- История

- Кинематография

- Компьютеризация

- Косметика

- Кулинария

- Культура

- Лексикология

- Лингвистика

- Литература

- Логика

- Маркетинг

- Математика

- Материаловедение

- Медицина

- Менеджмент

- Металлургия

- Метрология

- Механика

- Музыка

- Науковедение

- Образование

- Охрана Труда

- Педагогика

- Полиграфия

- Политология

- Право

- Предпринимательство

- Приборостроение

- Программирование

- Производство

- Промышленность

- Психология

- Радиосвязь

- Религия

- Риторика

- Социология

- Спорт

- Стандартизация

- Статистика

- Строительство

- Технологии

- Торговля

- Транспорт

- Фармакология

- Физика

- Физиология

- Философия

- Финансы

- Химия

- Хозяйство

- Черчение

- Экология

- Экономика

- Электроника

- Электротехника

- Энергетика

ПРАКТИЧЕСКОЕ ЗАНЯТИЕ

ПРАКТИЧЕСКОЕ ЗАНЯТИЕ

Тема: Введение лексического материала по теме «Бухгалтерские документы»

Содержание работы:

1.Чтение и перевод текста

2.Заполнение бухгалтерской документации

1.Чтение и перевод текста

Accounting is a system of gathering, summarizing, and communicating financial information for a business firm, government, or other organization.

Most accountants specialize in a field of accounting. The major fields include financial accounting, management accounting, tax accounting, auditing, and management consulting services.

Financial accounting involves the preparation of a business's financial statements, mainly for users outside the business. These reports are used by owners and potential owners of a business and by people who have loaned a company money. Some government agencies that regulate business and the stock market require companies to submit financial statements to them.

Management accounting helps managers plan and control a company's operations. Accountants prepare budgets to express management's goals in financial terms. After a budget has been adopted, performance reports compare actual results with the budget. Cost accountants help management keep track of how much it costs a company to make the product, or provide the service, it sells.

Tax accounting consists of preparing tax returns for organizations or individuals and determining the taxes involved in proposed business transactions. Tax accountants suggest ways to save money on taxes. They must have a thorough knowledge of the tax laws that affect their clients or employers. They also must know the details of court rulings in a wide variety of tax cases.

Auditing involves the examination of an organization's financial statements and records. CPA auditors from outside the organization provide assurance that the organization's financial statements present financial information fairly and that they follow generally accepted accounting principles. People use such statements in deciding which companies to invest in and lend money to.

There are several accounting documents kinds: primary (accounting), financial, settlement-monetary, organizational-administrative, statistical. Documents with information recorded in them ensure its accumulation, safety, the possibility of transmission, reusable use. They perform the function of continuous accounting.

The most common accounting documents are:

- statements, incoming and outgoing orders for the payment of money from the cashier's office;

- money orders;

- commodity checks, account and income invoices;

- power of attorney, contract;

- accounts;

- Acts of work performed and acceptance-transfer of goods;

- documentation for the issuance of material values;

- orders, orders, acts of audits, explanatory and memorandum notes, minutes of meetings, service letters, acts of commissions.

All of them are different in nature. By signing accounting documents, each employee assumes responsibility for the correctness of the design, expediency of the operation, reliability of the information reflected in them.

Accounting documents can be divided into 3 groups:

- incoming;

- outgoing;

- internal.

Incoming messages are received in one stream of documents and processed by a special worker. After receiving and verifying the correctness of the compilation and processing (the presence of seals and signatures), they are sorted into unregistered and registered and sent to the appropriate departments. Accounting documents, as a rule, are not registered. Accounting also receives a lot of data from other structural units.

Further processing of information carriers has its own specifics. The received documents are transferred to the employee, for which the relevant work site is fixed (material or financial activity, payroll calculation and others).

The employee checks the completeness and correctness registration of the primary document, the accuracy of filling in the details, the legality of the operation, the logical linkage of the indicators. Accepted documents are systematized in chronological order (by dates) and are made up by cumulative statements (memorial orders) or in accounting registers.

The order of the form of records of accounting accumulative documents is defined in the accounting instruction.

Registration of organizational and administrative information is carried out according to the rules of compiling official documents.

Checking and sending outgoing data is done in the general flow through the secretary or office.

When sending, check the correctness of the document (availability of date, seal, signature, all pages, correctness of the addressee).

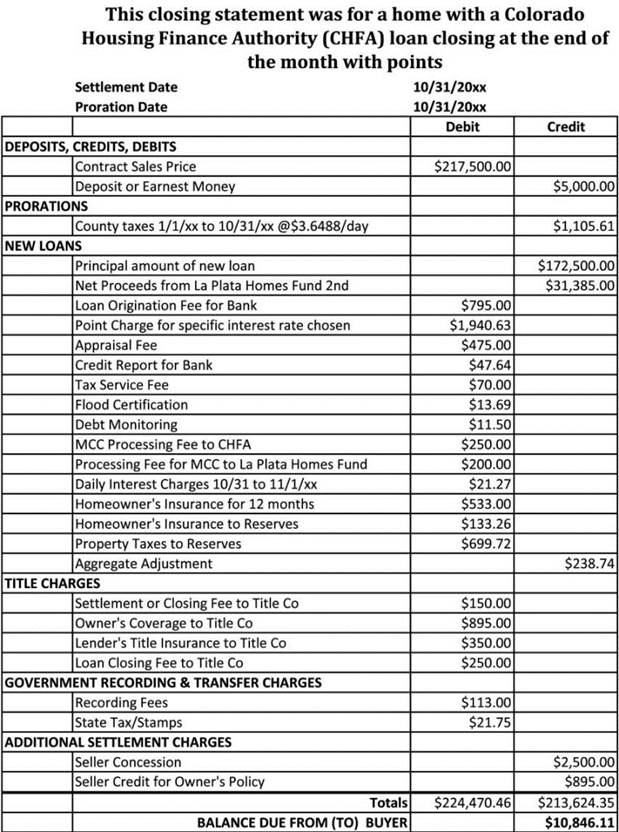

2.Заполнение бухгалтерской документации

|

|

|

© helpiks.su При использовании или копировании материалов прямая ссылка на сайт обязательна.

|